You’ll have to fold on cap when Bill comes back from Lords, PM warned www.standard.co.uk

Has Simon backed the wrong horse again? – Owl

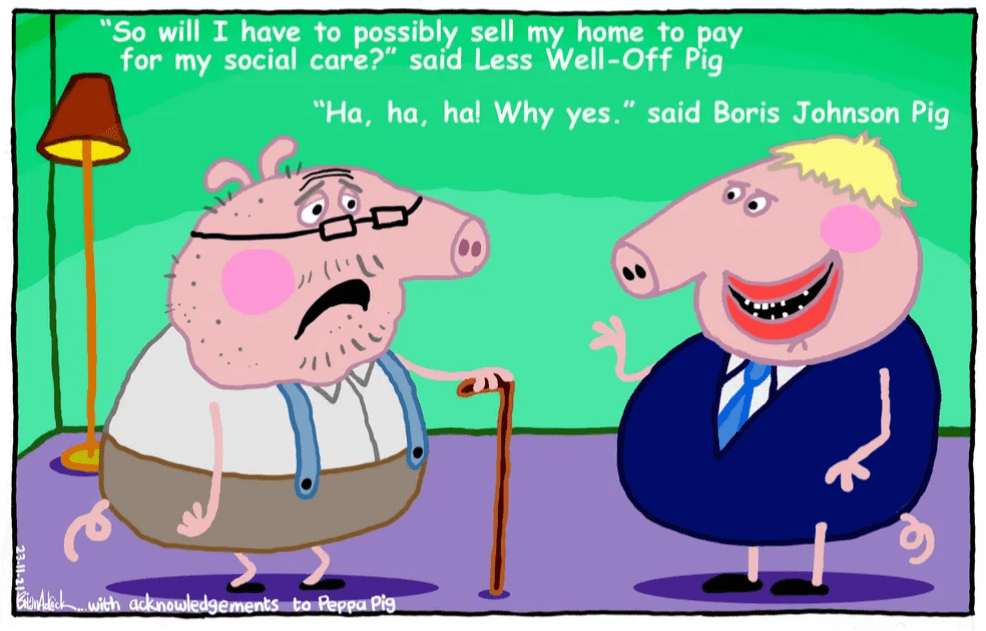

Boris Johnson’s social care reforms are grossly unfair

Editorial www.independent.co.uk

Ever been to Peppa Pig World?” the prime minister asked the bemused delegates at the CBI conference. Not many had, it seems, not least because of the Covid-19 lockdowns over the past 20 months or so, the imposition of which not being aided by Boris Johnson’s disastrous prevarications and confusions.

It was a low point, but perhaps a mercy to the assembled business folk that he got the pages of his speech mixed up, and stopped jabbering. At least the silence was comprehensible, punctuated only by some utterances of “forgive me”. Despite a vague commitment to “levelling up” as a “moral mission”, Mr Johnson was wise to avoid any reference at all to the government’s latest evolution of its social care policy. Which could easily be labelled it’s social “don’t care” policy.

It is effectively a tax policy reversed and turned upside down. It is eye wateringly, heartrendingly unfair. Rather than richer people (and their descendants) paying proportionately more for their care in old age or disability, or even the same as poorer families, it means that they will pay proportionally less. In its way, it is quite an achievement for an administration to come up with such a regressive policy and yet market it as a fair and equitable package of reforms. Flawed as it was before, it is now unacceptable.

It doesn’t do much for “levelling up” or social justice. Given the concentration of personal wealth in the south, the policy will exacerbate the north-south divide. The even more skewed cascade of unearned wealth down the generations will also increase the gap between rich and poor within every region. The financial impact of the social care policy is to entrench disadvantage and widen existing economic divisions. The property that the children of the already wealthy inherit will be rented out to the children of those who have seen their inheritance disappear in social care home fees. The final insult is that the new social care levy, as a form of national insurance, will be paid by the low paid, but not by the landlords living off their newly protected riches.

The new social care policy is nothing less than a powerful engine of inequality. According to Andrew Dilnot, who produced the original and best report on funding social care a decade ago, the less well off will derive little benefit from these changes, and the Treasury will save £900m, a small sum in the wider context.

It is policy being made on the hoof, and in the wrong direction. Having gifted the Labour Party sleaze to run with, now the prime minister has opened another early window on the advent calendar with the most obscenely unfair policy in decades.

Given the disquiet voiced by many Conservatives, precisely because of the potential electoral repercussions, the policy may yet have to be revised once again, and it would certainly not survive a change of prime minister or party of government, as Jeremy Hunt is hinting. It has unhappy echoes of the poll tax of the late 1980s – a well-meaning reform of an outdated and unpopular system, but one that somehow managed to make things more complex and more unfair.

Few noticed the implications of a complex new way of financing local government, naturally, but opposition grew as the details became clear, and then came the riots. The poll tax also inflicted huge political damage on the then Conservative government, and contributed to the fall of Margaret Thatcher (that and relations with Europe and an imperious style of government).

Mr Johnson should heed history, and perform one of his celebrated U-turns before his policy does any more capricious harm to older people and their families, and indeed himself as prime minister. Otherwise he’ll have all the time he wishes to spend at Peppa Pig World.