2019 in Britain:

1,249 McDonald’s

500 Burger King’s

500 Starbucks

over 2,000 Food Banks

2019 in Britain:

1,249 McDonald’s

500 Burger King’s

500 Starbucks

over 2,000 Food Banks

A VOTE FOR ANYONE OTHER THAN CLAIRE WRIGHT IN EAST DEVON MEANS YOU HANDED YOUR VOTE TO CONSERVATIVES WHICHEVER PARTY YOU VOTED FOR – ONLY CLARE WRIGHT CAN DEFEAT THEM – VOTE TACTICALLY UF YOU DO NOT WANT JUPP TO RETAIN SWIRE’S SEAT

Essential watching before making your election choice on Thursday. For those of you who can, please circulate as widely as possible.

REMEMBER – VOTING FOR ANYONE BUT TIRELESS NHS CAMPAIGNER CLAIRE WRIGHT WILL BE A VOTE FOR FURTHER KILLING OFF OF THE NHS – AND US:

Philip Algar is an active campaigner in his local town of Ottery St Mary.

HARD TIMES, HARD LUCK

Austerity, anger and adventure

by Philip Algar

“In his latest book, local author Philip Algar paints a sympathetic picture of the fictional Devon village of Woodfield Magna. Like so many across the country, it is decaying. The young people, lacking local employment, affordable homes and public transport, are moving away. Those who remain, mainly the elderly and financially challenged, are confronted by the closure of local hospitals, libraries, bus routes and social services and by more crime and other challenges reflecting the government’s austerity plan.

The locals discuss serious matters, such as whether the name of the pub should be changed, and lesser topics such as global warming, but their efforts to publicise their plight, on television, reveal a government plot to curb free speech.

One elderly resident, whose pension is lower than it should have been, because of the suspect actions of a very dubious businessman, dubbed the ugly face of capitalism, needs an operation to eliminate constant pain. The NHS will not assist for some time and he cannot afford to use the private sector. He and his friends, trying to help him, become involved in an unlikely adventure that emphasises the problems that millions face and which captures the interest of the entire nation and the attention of the government.

This satirical story, characterised throughout by a sustained and quiet humour, paints an understanding picture of village life and mocks many aspects of contemporary society.”

HARD TIMES, HARD LUCK (ISBN number 978-0-244-53385-4) is available from The Curious Otter Bookshop 10 Mill Street, Ottery St. Mary EX11 1AD price £8.99 or from the author direct on philipalgar@btinternet.com at the same price, including postage and packing to UK addresses.

“The Institute for Fiscal Studies is deeply unimpressed at what it deemed a “lack of significant policy action” in the Conservative Party manifesto.

The Tory social care crisis for Britain’s elderly and infirm that Johnson had promised to fix when he became PM did not even get a mention in the manifesto. Johnson had previously claimed that he had a plan ready to sort it out.

The IFS concluded that the manifesto plans meant people expecting relief for Britain’s public services after a decade of austerity would instead see “cuts to their day-to-day budgets of the last decade baked in.”

Economic researchers at the independent think tank calculated that the National Insurance threshold rise to £9,500 that Boris Johnson appeared to have lied or been mistaken about will actually only save most in paid work “less than £2 a week” and highlighted the “notable omission” for any plan to deal with the crisis in social care funding.

Nigel Edwards, chief executive at the Nuffield Trust, an independent health think tank, said he was “bitterly disappointed” to see “unnecessary delay” in tackling the issue of social care.

IFS director Paul Johnson said: “If a single Budget had contained all these tax and spending proposals, we would have been calling it modest.

“As a blueprint for five years in government, the lack of significant policy action is remarkable.”

Main manifesto pledges quickly debunked

Speaking at a launch event in Telford, Boris Johnson reaffirmed his commitment to take the UK out of the EU by the end of January, so they could “forge a new Britain”. “We will get Brexit done and we will end the acrimony and the chaos,” he said.

As well as a flagship promise of 50,000 more nurses for the NHS in England despite Brexit “chaos”, the manifesto included a U-turn restoring maintenance grants for student nurses previously scrapped by the Tories.

Tory sources later acknowledged that about 30,000 of the additional nurses would come from measures to retain existing staff rather than new recruits, and the main Tory manifesto pledge was debunked among other claims by a fact checking service within hours of the launch. Labour called the Tory figures “deceitful.”

Chief executive Will Moy said the Conservative Party could “do more to meet the standards we expect” after investigating its pledges on paving the way for 50,000 new nurses and limiting day-to-day spending increases to only £3 billion, despite promising a litany of public services investment.

The fact checkers also slammed Johnson’s use the the slogan “get Brexit done”, a phrase that appears 22 times in the manifesto including on the cover, when a deal with the European Union could take “years to negotiate”.

“The Brexit process will not be completed by January,” despite what Johnson keeps repeating said the independent organisation.

‘Older people face a triple whammy’

“After a decade of the Conservatives cutting our NHS, police and schools, all Boris Johnson is offering is more of the same: more cuts, more failure, and years more of Brexit uncertainty,” Jeremy Corbyn responded.

He added: “Boris Johnson can’t be trusted. Older people face a triple whammy as he has failed to protect free TV licences for over 75s, refused to grant justice to women unfairly affected by the increase in the state pension age, and not offered a plan or extra money to fix the social care crisis.”

The lacklustre manifesto may be down to Conservative complacency after recent polls. The latest polling released on Sunday, created by Datapraxis using YouGov polling and voter interviews, suggested the Tories were on course to secure their largest Commons majority since 1987 – a majority of almost 50 MPs.

This would mean if Boris Johnson met the public services spending promises in his manifesto the UK would still be looking at a decade of cuts “baked into” our services, according to the IFS analysis.

Boris Johnson’s broken promise to fix Tory social care crisis

Paul Johnson of the IFS’ initial reaction to the Tory manifesto was scathing: “If the Labour and Liberal Democrat manifestos were notable for the scale of their ambitions the Conservative one is not. If a single Budget had contained all these tax and spending proposals we would have been calling it modest. As a blueprint for five years in government the lack of significant policy action is remarkable.

“In part that is because the chancellor announced some big spending rises back In September. Other than for health and schools, though, that was a one-off increase. Taken at face value today’s manifesto suggests that for most services, in terms of day-to-day spending, that’s it. Health and school spending will continue to rise. Give or take pennies, other public services, and working age benefits, will see the cuts to their day-to-day budgets of the last decade baked in.”

“One notable omission is any plan for social care. In his first speech as prime minister Boris Johnson promised to ‘fix the crisis in social care once and for all’. After two decades of dither by both parties in government it seems we are no further forward.

“On the tax side the rise in the National Insurance threshold was well trailed. The ambition for it to get to £12,500 may remain, but only the initial rise to £9,500 has been costed and firmly promised. Most in paid work would benefit, but by less than £2 a week. Another £6 billion would need to be found to get to £12,500 by the end of the parliament. Given the pressures on the spending side that is not surprising.”

“Perhaps the biggest, and least welcome, announcement is the ‘triple tax lock’: no increases in rates of income tax, NICs or VAT. That’s a constraint the chancellor may come to regret. It is also part of a fundamentally damaging narrative – that we can have the public services we want, with more money for health and pensions and schools – without paying for them. We can’t.”

School cuts barely reversed

The Conservative manifesto confirmed previous commitments in England to increase school spend in England by £7.1 billion by 2022–23. However, that would leave spend per pupil in real terms after a decade of austerity at the same level as 13 years ago, the IFS explained.

In contrast the IFS found the Labour commitment of a £7.5 billion real terms increase by 2022–23 a 14.6% rise in spending per pupil.

Unlike Labour and the Liberal Democrats the Conservative manifesto refused to extend free, pre-school childcare.

IFS researchers warned that the Conservative manifesto pledges left “little scope for spending increases beyond next year outside of those planned for health and schools.”

In a dire warning the IFS added: “even in 2023–24 day-to-day spending on public services outside of health would still be almost 15 per cent lower in real terms that it was at the start of the 2010s.”

@BenGelblum

IFS warn austerity ‘baked in’ a Tory manifesto with ‘notable’ lack of social care funding

“The UK has one of the most extreme forms of capitalism in the world and we urgently need to rethink the role of business in society. That’s according to Prof Colin Mayer, author of a new report on the future of the corporation for the British Academy.

Prof Mayer says that global crises such as the environment and growing inequality are forcing a reassessment of what business is for.

“The corporation has failed to deliver benefit beyond shareholders, to its stakeholders and its wider community,” he said.

“At the moment, how we conceptualise business is, it’s there to make money. But instead, we should think about it as an incredibly powerful tool for solving our problems in the world.”

He said the ownership structure of companies had made the UK one of the worst examples of responsible capitalism.

“The UK has a particularly extreme form of capitalism and ownership,” he said.

“Most ownership in the UK is in the hands of a large number of institutional investors, none of which have a significant controlling shareholding in our largest companies. That is quite unlike virtually any other country in the world, including the United States.”

This heavily dispersed form of ownership means none of the owners is providing a genuinely long-term perspective on how to achieve goals while also making money.”

It’s what people voted for when they voted Conservative for continued austerity.

“A quarter of Devon’s children are living in poverty once housing costs taken into account.

More than 35,000 children in Devon are living in poverty once housing costs are taken into account, councillors have heard.

A Children’s Services Self-Assessment went before Devon County Council’s Children’s Scrutiny Committee last Monday which provided an up-to-date evaluation of the needs of children and families in Devon.

The report outlined how 14 per cent of the local authority’s children are living in poverty (before housing costs), but that rises to 25 per cent (after housing costs) are taking into account.

More than 10 per cent of children are entitled to free school meals, the report added, and also says that 41,000 households in the county are affected by fuel poverty.

Cllr Rob Hannaford, chairman of the Children’s Scrutiny Committee, said that the figures were shocking and in many areas, including Devon, growing up in poverty is not the exception but the rule.

Commenting on the report after the meeting, he said: “These local figures for child poverty in Devon are truly shocking, and it’s completely unacceptable and wrong in 2019, in one of the richest countries in the world, that we are still dealing with this most basic of issues affecting so many children.

“Large numbers of people seem to just wrongly assume that because we live a beautiful part of the country, that we don’t experience the same serious social problems that other areas do. These new figures again show in stark reality that this is just not the case, and much of our poverty and hardship is hidden by the affluence that some others have.”

Cllr Hannaford added: “Thousands more families across Devon, are living on the cusp of the poverty line. One unexpected setback – like redundancy or illness – could push them into the poverty trap.

“Overall there are more than four million children in the UK growing up in poverty. The situation is getting worse, with the number set to rise to five million by 2020. And those poverty rates have risen for every type of working family – lone-parent or couple families, families with full and part-time employment and families with different numbers of adults in work. This is the first time in two decades this has happened, and incredibly it is happening at a time of rising employment, and these figures in Devon are in line with these trends.

“But the evidence is clear – poverty can make existing vulnerabilities worse. Growing up in poverty puts at risk the building blocks of a good childhood – secure relationships, a decent home, having friends and fun, and an inspiring education.

“A child is said to be living in poverty when they are living in a family with an income below 60 per cent of the UK’s average after adjusting for family size. So it’s just not acceptable that some people still seem to trot out the same old tired response that no one is really in poverty these days, and it’s like Victorian times or the 1930s, such as when children didn’t have shoes on their feet.

“My grandparents were brought up in near slum conditions, and at times they also did not have proper shoes, and went hungry, are we really seriously saying that we want to inflict all this misery and hardship on children today?”

He continued: “Clearly the biggest driver for children’s poverty nationally and locally is the profound lack of social, affordable, decent housing. The figures are stark. 120,000 children in England are living in temporary accommodation. There are also 90,000 children living in families who are ‘sofa-surfing’. And of course this accommodation is usually terrible.

What is poverty in the UK?

“B&Bs where sometimes the bathroom is shared and there is nowhere to cook. Places where vulnerable adults can be living on the same corridor. Office block conversions – individual flats the size of a parking space, where families live and sleep in the same single room. And even converted shipping containers – cramped and airless – hot in the summer, freezing in the winter. This is a reality that shames the whole nation.

“Rising living costs, low wages and cuts to benefits are creating a perfect storm in which more children are falling into the poverty trap. Shockingly, two thirds of children living in poverty have at least one parent in work. Many families are struggling to cope with the rising cost of living. The prices of essentials like food and fuel are going up and this hits Britain’s poorest families hardest. We know that parents are skipping meals so they can afford to feed their children, and in winter many families are forced to make the impossible choice of feeding their children or heating their homes.

“So we know what actually causes child poverty and we know how to end it. We know that the income of less well-off families has been hit by severe real-terms cuts in benefits and by higher housing costs. And we know that work does not always guarantee a route out of poverty, with two thirds of child poverty occurring in working families.

“Yet in many areas, including Devon, growing up in poverty is not the exception, it’s the rule, with more children expected to get swept up in poverty in the coming years, with serious consequences for their life chances. Policy makers can no longer deny the depth and breadth of the problem, and the Government must respond with a credible long term child poverty reduction strategy.”

The report revealed that in primary schools, 10.9 per cent of pupils are entitled to free schools meals, and 10 per cent in secondary schools, but Cllr Hannaford feared that the numbers were in reality much higher.

He added: “The percentage is shocking, but there is a feeling in rural areas that it may be more as there is a stigma about people and they don’t claim it so they don’t have the finger pointed at in the local community.”

Cllr Margaret Squires, who represents the Creedy, Taw & Mid Exe ward, added her concerns to those of Cllr Hannaford.

She said: “A headteacher who had moved down here from London said to me the deprivation they see is different. Down here, people don’t want others to know they have free school meals, so they are working every hour they can. But it means that the children are missing out as the parents are so tired, they haven’t got the time to sit and listen to them read.

“I my area, we are virtually fully employed, but some of them work two jobs so they can live in the area, and to survive, they are working all these hours, but it not recorded as deprivation as they don’t have time to sit and read with their children.”

The figures in the report showed at as of September 1, 2019, 771 children were being looked after by the council – a rate of 54.8 per 10,000 children – an increase from 750 – 52.2 per 10,000 children – at March 31.

At September 1, 2019, 3,219 children had been identified through assessment as being formally in need of a specialist children’s service, an increase from 3,318 in March 2019, but the number of children subject of a child protection plan had decreased from 518 to 505 between March and September.

The report also said that there were 25 unaccompanied asylum-seeking children in the area, and that eight children and young people who turned 18 years old and who were in the care of the local authority were living in unsuitable accommodation during 2018-19.

Cllr Linda Hellyer questioned what the council was doing about it, why they were unsuitable, and what have we done to get them somewhere better.

In response, Darryl Freeman, Head of Children’s Social Care, explained that the definition of unsuitable included prison, where two of the eight were in custody. He added that the council will continue to work with them, assuming they allow them to remain in touch, and to ensure that they have choices once they leave custody.

The report also added that the top three risks for the future were increase in demand, across all services, recruitment and retention, particularly of experienced social workers, and sufficiency of provision for special needs children and placements for Children in Care.

The council also earlier this year adopted a new Children and Young People’s Plan, which is the single plan to co-ordinate developments for the next three years

Each priority in the plan has a detailed strategy/ action plan below it with a multi-agency group led by a senior manager from the partnership.

The self-assessment report was noted by the committee.

https://www.devonlive.com/news/devon-news/child-poverty-devon-truly-shocking-3579939

Claire Wright has been clear with her manifesto – protecting what is best about East Devon, standing up for the NHS am]nd social care, conserving the environment and improving education and inequality.

Click to access GEManifesto2019FINAL5.pdf

Unfortunately, the Conservative Party has not been so clear.

Other party manifestos are unimportant in East Devon.

A vote for anyone other than Claire Wright is a vote for the Tories.

Our parachuted-in, Tory apparatchik candidate is throwing himself around the constituency like a whirling dervish (mostly accompanied by the same old 5-6 people – who must be finding it quite tiring) But has anyone asked him these questions and, if so, has he given any answers?

If not, maybe hustings will provide a platform for him to answer.

What do you think of the Tory fake-news “factcheck uk” Twitter account? Is that acceptable?

What do you think of the “50,000 more nurses” which includes 19,000 that you think you might be able to persuade NOT to leave? Is this acceptable?

What do you think about the “20,000 more police” when you got rid of 21,000. Is this acceptable?

What do you think of the “60 new hospitals” when itis actually only 6 – the others to get minimal funding to plan new hospitals, not build them? Is this acceptable?

Why has social care been left out of the manifesto? Is this acceptable?

All the above is said to be taking 10 years to achieve – if at all? Is this acceptable?

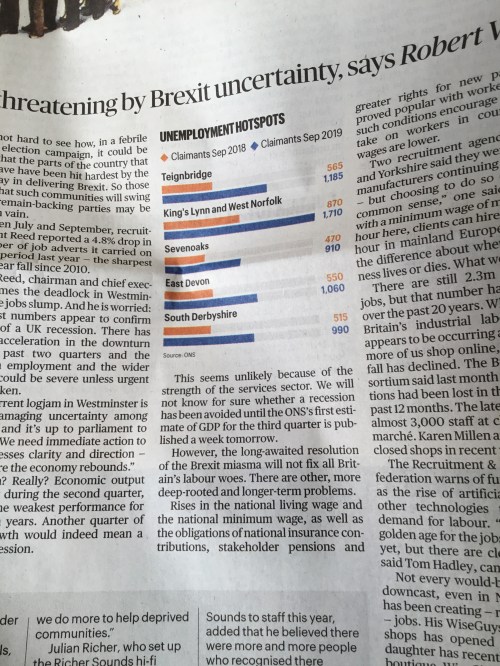

Sunday Times article on new unemployment areas – high street decline, business rate penalties, jobs moving abroad and reduced demand for labour due to automation are some reasons given. Owl would like to see the breakdown per town – oldies in some towns, unemployed youngsters in others …

Does anyone else find it distasteful to say the least that the party that shafted the poor, brought the NHS to its (broken) knees and took 20,000 police officers off the street now says it will increase benefits, is funnelling short-term money into the NHS before a pre-election crises and promises to return SOME of those police officers to the streets is the one that caused all these problems in the first place?

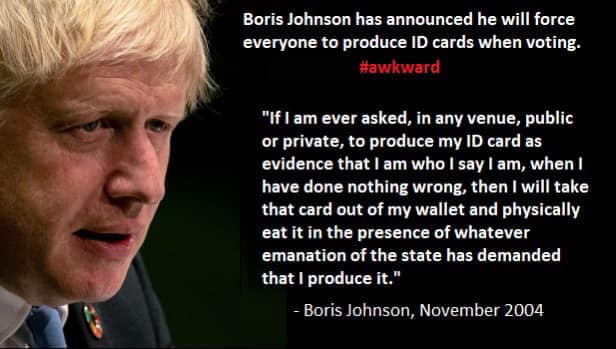

“This week’s Queen’s Speech revived proposals to introduce photographic ID requirements for voting in British elections. The Democratic Audit team assess the available evidence on the likely consequence of such a measure, and consider whether the legislation tackles the right priorities for improving our elections on which there is consensus, or suggests moves to enhance Tory election chances via excluding voters presumed unfavourable to them….”

And remember – you can’t just turn up at a foid bank: you have to be referred by a doctor, social worker and the like. And many recipients are from working families.

“The number of people using food banks in Devon has hit a record high, and Universal Credit has been blamed for contributing to the problem.

Figures provided by the Trussell Trust, a charity that works to end the need for food banks in the UK, more than 24,000 emergency food parcels were issued to people in need across our county in 2018/19.

One in three of these food parcels, or 8,242, was for a child.

Campaigners say “enough is enough” and warned Universal Credit is adding to the huge numbers of people who don’t have enough money to “cover the basics” such as food. …”

https://www.devonlive.com/news/devon-news/food-bank-users-devon-reach-3422071

“Broadclyst school [photograph from article above]in Devon has a specially built classroom where 67 children are taught simultaneously. Though unions say such class sizes are detrimental to learning, the school’s head teacher insists pupils are offered an “excellent education”.

It looks more like a lecture theatre than a primary school classroom. Welcome to Broadclyst Community Primary School in Devon, where year 6 pupils are taught in a class of 67 — sometimes with just one teacher.

A Sunday Times investigation has found that cash-strapped primary schools are packing pupils into giant classes to boost their budgets. A school receives between £3,500 and £5,000 a year for each child. More than 559,000 primary pupils were taught in “super-size classes” averaging more than 30 children last year, compared with 501,000 five years earlier, according to our analysis of official data.

In parts of northwest England — including Oldham, Bury, Trafford and Tameside — a quarter of primary children are being taught in such big classes, as per-pupil funding encourages heads to fill their classrooms.

It is illegal to teach children under the age of seven in classes of more than 30 pupils, but there are no such rules for older children. But we have found that nearly 5% of pupils aged 5-7, roughly 73,000 children, were taught in classes of more than 30 last year. Some heads use just one teacher for occasional classes of more than 60 pupils. Broadclyst has one of the highest average class sizes, 42, and at times teaches 67 older children together in a specially built room.

Teaching unions and experts have always warned that such big class sizes damage children’s education. But this weekend Jonathan Bishop, Broadclyst’s head teacher, defended the policy, insisting that the school, about five miles northeast of Exeter, offered an excellent education, and class size “was not the big factor” in a good-quality education.

The school is rated as “outstanding” by the regulator Ofsted.

Bishop said: “I do not think 30 is a magic number to get better-quality education. It is not class size that dictates the quality of education. Our year 6 classroom has got 67 children in one room. There are times when one teacher teaches those 67 children. Is that wrong? Of course it is not wrong.

“Our year 6 classroom is designed like a lecture theatre: I can seat 67 children in there. I know I will be public enemy No 1 by saying this.”

Experts warned that the UK was moving inexorably towards the giant classes found in parts of Asia.”

Source: Times (pay wall)

“The top 1% of high earners in the UK have enjoyed a 7.6% real terms pay increase over the last two years, while the average worker’s pay rose by just 2p an hour.

A TUC analysis of government hourly pay data between 2016 and 2018 shows thatpay among the very top earners increased at a faster rate than any other group.

People in the top bracket saw their pay increase by an average of 7.6% from £58.73 in 2016 to £63.18 in 2018, according to the Office for National Statistics (ONS) annual survey of hours and earnings. Over the same period, the real terms pay of average workers rose by just 0.1% or 2p to from £12.71 to £12.73.

The TUC said that average pay in real terms, when adjusted for inflation, was still worth less in real terms than before the financial crisis continuing the biggest squeeze on wages since the end of the Napoleonic Wars.

Frances O’Grady, general secretary of the TUC, warned that the gap between the richest and everyone else will continue to widen under the prime minister, Boris Johnson’s planned tax cut for high earners, which will cost the Treasury £9.6bn a year, according to the Institute for Fiscal Studies (IFS).

“While millions struggle with Britain’s cost of living crisis, pay for those at top is back in the fast lane,” O’Grady said. “We need an economy that works for everyone, not just the richest 1%. Boris Johnson’s promised tax giveaway to high earners would only make things worse. The prime minister is focused on helping his wealthy mates and donors, not working people.” …

“A decision by Barclays to pull out of an agreement allowing bank customers to withdraw cash from post offices for free has been criticised as “shocking”.

The bank is the only one to scrap over-the-counter cash withdrawals at Post Office branches, with 28 other UK banks signing up to a new deal that means millions of people can continue to benefit from free access to everyday banking services.

The move by Barclays prompted a wave of criticism, including from a regulatory body, and appears to be linked to a sizeable rise in the bank-funded fees paid to postmasters for providing these services. Barclays has separately announced its own proposals, which it said were designed to boost bank branch demand and improve access to cash. …”

The south-west, as usual, gets least funding, and, of course, Cranbrook, with no town centre at all, is NOT historic!

“Historic English shopping centres will benefit from a £95m regeneration fund, the government has said.

In all, 69 towns and cities will receive money, with projects aimed at turning disused buildings into shops, houses and community centres.

The largest share of money, £21.1m, will go to the Midlands, with £2m going to restore buildings in Coventry that survived World War Two bombing.

The government said the move would “breathe new life” into High Streets.

The government’s Future High Street Fund is providing £52m of the money, while £40m will come from the Department for Digital, Culture, Media and Sport (DCMS). A further £3m is being provided by the National Lottery Heritage Fund.

Towns and cities had to bid for the £95m funding, which was first announced in May.

The announcement comes after figures showed that about 16 shops a day closed in the first half of the year as retailers restructure their businesses and more shopping moves online.

Lisa Hooker, consumer markets leader at PwC which was behind the research, said retailers had to invest more in making stores “relevant to today’s consumers”, but added that “new and different types of operators” needed encouragement to fill vacant space.

‘Wider regeneration’

The government said the money would “support wider regeneration” in the 69 successful areas by attracting future commercial investment.

“Our nation’s heritage is one of our great calling cards to the world, attracting millions of visitors to beautiful historic buildings that sit at the heart of our communities,” said Culture Secretary Nicky Morgan.

“It is right that we ensure these buildings are preserved for future generations but it is important that we make them work for the modern world.”

Other major projects include a £2m drive to restore historic shop-fronts in London’s Tottenham area, which suffered extensive damage in the 2011 riots.

By region, the funding breaks down as follows:

London and the South East: £14.3m

South West: £13.7m

Midlands: £21.1m

North East and Yorkshire: £17.2m

North West: £18.7m

You can read a full list of the towns and cities that will benefit here

https://www.bbc.co.uk/news/business-49692091

but for south-west:

Chard

Cullompton

Gloucester

Keynsham

Midsomer Norton

Plymouth

Poole

Redruth

Tewkesbury

Weston-Super-Mare

“Increasing competition from online outlets is putting High Streets across the country under growing pressure,” said the DCMS.

“As part of the government’s drive to help High Streets adapt to changing consumer habits, the £95m funding will provide a welcome boost.”

Responding to the move, shadow culture secretary Tom Watson said High Streets had been “decimated” by “a decade of Tory austerity”.

He added: “This funding pales in comparison to the £1bn Cultural Capital fund that Labour is committed to, which will boost investment in culture, arts and heritage right across the country, not just a few lucky areas.”

“The number of families at risk of becoming homeless has risen by more than 10 per cent as councils struggle to support people living in overcrowded accommodation or facing eviction.

In the first three months of this year 70,430 households were judged to be on the brink of being made homeless, up from 63,620 in the previous quarter, the latest figures showed.

Local authorities have placed 84,740 families and couples in temporary housing, including 126,020 children, the highest figure in a decade.

A report last month by Anne Longfield, the children’s commissioner for England, showed that thousands of children were living in converted shipping containers and office blocks after being classed as homeless.

Yesterday’s figures were published by the Ministry of Housing, Communities and Local Government a year after rules came into effect requiring councils to do more to prevent people from becoming homeless. It doubled to 56 days the period over which they must assess a person’s risk.

The most common reason for people becoming homeless, affecting 18,150 households, was family or friends no longer being willing to provide temporary shelter. The second most frequent cause was the termination of a shorthold tenancy by the landlord, which applied in 14,700 cases.

Kate Henderson, chief executive of the National Housing Federation, which represents housing associations, said more homes should be built for rent by people on low incomes rather than for better-off private buyers.

“It is unacceptable that the number of families living in temporary accommodation has been allowed to reach an eight-year high with no real action to tackle the root of the problem,” she said.

David Renard, the Local Government Association’s housing spokesman and Conservative leader of Swindon borough council, welcomed extra funds announced in the budget to support homeless people but said that long-term funding was needed.

“A lack of affordable housing has left many councils struggling to cope with a rising number of people coming to them for help and are having to place more families and households into temporary and emergency accommodation as a result,” he said.

Luke Hall, a housing minister, said the Homelessness Reduction Act, which came in last year, was “helping people earlier so they are not having to experience homelessness in the first place”. He said the latest figures showed that progress was being made. “There is still more to do, though, which is why we have committed a record investment to ending homelessness and rough sleeping for good.”

The government published a separate report which showed that the number of vulnerable people sleeping rough had fallen by one third.”

Source: Times (pay wall)

Image from DevonLive article cited below:

https://www.devonlive.com/news/devon-news/how-perfect-devon-town-gained-3267664

Ian Hall (EDDC and DCC councillor for Axminster) has got himself in the news a lot recently with many, many press releases.

He wants all councillors to have (minimal) Disclosure and Barring Service checks at their own expense (even though the council’s officers say it is unnecessary and pointless).

Now, in an article that labels Axminster as “Crackminster” he declares himself an expert in “county lines” drug supply to the town. And disses “incomers” blaming them (and other feckless residents) for the town’s problems.

Rather than look at his town’s problems caused by Tory austerity (closed shops, closed sixth form at the school, closed factory (at which he once worked), large clone estates at every corner with no new facilities, closed community hospital beds, part-time police coverage … all the indications of deprivation and inequality .. . Who does he blame? He he blames the incomers that his party encouraged with its current and future overdevelopment and people who, he says, lack the community ethic and are workshy:

… “Axminster is a wonderful friendly town,” he says. “There is a tipping balance and it only takes one or two coming into the local area to tip the balance. But if they are coming here and adding something to the community I am all for it.” …

… [Ian Hall] says the town needs people who are prepared to work and buy into the community ethic and doesn’t have much time for those that don’t. …”

The article goes on:

“… House prices in Axminster tend to be higher than across the border but wages lower. Ian now travels to Chard in Somerset every day to work, making components for vacuum cleaners. A trip of just 14 minutes. … “

Smacks of ideas well above his party’s reduced police force and closed police stations to Owl. If house prices are high and wages low – who is to blame? Not the incomers who seem to be able to afford the houses with the loans given to them by his party, and who presumably also go to Chard and Exeter to work.

Oh, AND he’s on the town’s Regeneration Board, so he can do something about all these things!

Suddenly, he”s popping up everywhere and has (mainstream, very, very Tory or further right) ideas about everything are everywhere.

So – Police Commissioner? Next Leader of EDDC or DCC? Run against Neil Parish? Ruler of the Universe?

Whatever it is, if dissing his own town and blaming it on lack of community spirit and idleness of some of its residents will get him there – that will be fine, it seems.